|

| From Upside/downside graphs |

|

| From Upside/downside graphs |

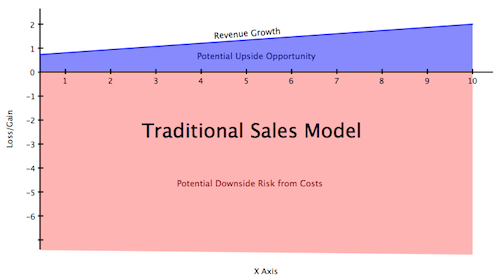

Over the years, Reid Hoffman and I have talked a lot about venture investing and the things that make people successful in startups. Reid likes to doodle a little graph on paper napkins about downside vs. upside focus and I thought I'd expand that a bit and share.

Normal sales oriented companies and organizations have sales that grows month on month if the organization is doing well. While there is a tremendous amount of energy spent on increasing sales, typically sales are capped by some reasonable growth rate over time.

On the other hand, the downside of a company is nearly unlimited. Projects can cost nearly an infinite amount of money if mismanaged and there are a myriad of risks that can cost an operating company tons of money.

The larger and more established the company, the more the organization, as a whole seems to be focused on mitigating risk and minimizing costs as a way to increase earnings and protect itself.

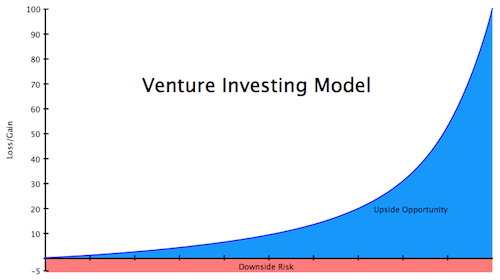

Venture investing, on the other hand, is typically a fund or an individual with relatively limited downside. The most that you're going to lose is the money you've invested and your time.

The upside in venture investing, however, is hugely leveraged. If you're in a good deal, you can make hundreds and thousands times your money with very little incremental cost. The key is to make sure you're in the right deals and that those companies that will potentially knock the ball out of the park get all of the help and support that they need to maximize their chance of success.

In fact, most successful investors spend the majority of their time working on their successful portfolio companies and very little time on the companies that are doing poorly.

In many cases, the companies that are doing poorly need the most help and the intuition is to focus on protecting our investments. Many investors spend all of their time helping their poorly performing companies.

I think that the training from traditional businesses causes people to focus on minimizing the downside instead of single-mindedly focusing on the upside. However, in a venture investment, the MOST you will lose is the money you have invested. Getting 1 million of the 5 million that you invested back from a liquidation is not nearly as important as making sure you're in the next big hit and that the investments that have potential achieve their potential and find their acquirers and partners.

This also influences the way people negotiate contracts. A few percentage points or deal points here and there can damage, slow down or destroy relationships and businesses. Trying to get every last percentage point out of a transaction with a startup is fighting over something that's worth zero if the company isn't successful. It's much more likely to increase your chance of making money if you're helpful and supportive than if you've pushed the entrepreneur against the wall and taken every last percentage point out of the deal that you can from them.

It's stupid to be a sucker and it's not prudent to be sloppy, but squeezing entrepreneurs unnecessarily for that extra nickel isn't worth it when the probability of upside is what you're trying to increase and having more rights in a failure is really not going to make you rich.

I think that all good investors understand this focus on upside vs. downside and I struggle with partners, co-investors and entrepreneurs who seem to live in a downside minimization model. Downside minimization may save you money here and there, but over the long run, will never really provide the kind of returns that an upside oriented model will.

Great post,

Love the graphic for the first point and the articulation of the second point.

Re the second point, I made that argument to a VC last night...

"If you told me you needed those terms [cumulative dividends and participating preference], I'd understand (you don’t *really* like my deal) and move on. because even in a liquidation, you want to still be able to go for dinner with the other side and maybe even do another deal, both the wiser. That’s hard to do when you end up in a liquidation for twice the amount of your investment and you end up with 95% of the cash before legal and accounting fees suck up the rest. You may find yourself getting better exits from better companies using my terms, that you would have otherwise lost with your terms."

I never thought about investing in this framework before. The way you explain it, it's like running the house, instead of playing blackjack. Risk on both sides, but usually it's better to be one than the other.

Thanks.

The problem with those graphs is that the X-axes are the same. The top one is presumably 10 time units. Is the bottom one 10 time units, or 10 investment opportunities? It doesn't really matter. The point is that the X-axis on the bottom graph could in reality take 100 or 10,000 units to get the results wanted. So in the end, the red area could be many times greater than the red area in the top graph. And the green area in the top graph could be greater than that in the bottom graph, over a reasonable, non-infinite period of time or number of investments.

At any rate, apples and oranges.

Hey Mike. You're right. The units are apples and oranges, but I'm trying to show shape of focus, not some measurable amount of money or time.

Also, I didn't do it very clearly, but the point is that in the second graph, even if the downside is large, it is mostly capped whereas the top graph it really is unlimited.

My view is that downside protection is more important in "traditional" investing (Don't lose money).

Venture capital investing is generally acknowledged as a positive black swan oriented call option and as such the upside can be unlimited. Not sure if this point isn't clear to anyone who has spent some time either in the VC industry or thinking about the economics of the industry.

It is true the venture investing model's risk is finite, but failure is much more likely to occur. The graphs don't capture the likelihood of failure, just the cost of failure.

The second graph seems to depict one venture investment, not an entire portfolio. Wouldn't a portfolio graph look more like the traditional graph, hopefully with a steeper upside opportunity curve?

Steve:

Yeah, I guess the curve could be steeper, but with a good investor, the area under the curve should be larger than the downside. Not sure what you mean but traditional graph, but I think a portfolio return distribution would look like a power-law curve with a HUGE #1, smaller #2, and a lot of flatline towards the tail.

Very interesting post Joi... I enjoyed your explanation and the disucssion last night at the event held at SMU. I agree with your point of limited vrs limitless - It has a completely different feel.

I agree with your central arc of course, but I think you've mixed metaphors to make your case. First, this point in history is relatively unique. Prior to the Internet, email, online collateral, web conferences, and RSS feeds, the closest thing to an email blast was MailMerge requiring printer, paper, ink, stamps, and labor to stuff, seal, stamp, and mail them. Sales models were based on phone introductions and personal meetings. Trade shows happened once or twice a year, where web conferences are now possible on a moment's notice. You mailed disks or a tape - certainly didn't tell customers where to download software. If we accept pre-Internet as the basis of traditional mode, the fixed rectangle of expenses is actually too generous. Unless customers tend toward larger and larger deals or the amount of time required to close a sale keeps shrinking, revenue from a fixed size sales team will saturate and you'll have to add staff to keep the growth going, thereby expanding the downside risk.

Second, venture investors aren't really interested in the mainstream and decline segments of the market model, they're ears perk up for opportunities in the innovator and early adopter stages. Why? Because products and technology, no matter how unique, eventually become commoditized and the market values of companies selling commodities aren't nearly as compelling as those for whom the world is still their oyster. The VC's ideal exit point is probably somewhat left of the upside inflection in Rogers Adoption/Innovation Curve where excuses can be made that revenue is still growing exponentially (even if it has in fact leveled out) and they get maximum Price/Earnings for their holdings. So, some of the difference between the curves is due to which stage of the Rogers Adoption/Innovation Curve you're on. Venture capitalists don't stick around for the later stages - never see growth rates close to the consumer price index.

The second graph expresses the acceleration of a system(s). Such acceleration does not happen as a result of an accretive process of improvement such as is expressed in the first graph. The second graph expresses what happens with true investment success, which is that NEW processes are added—new ground is broken. Every natural system in status quo can be massaged for improvement, but such improvement is only incremental. When seeking a place to invest one’s resources, one should look beyond the present state of affairs and ask himself about the investee’s potential for, and comfort with change itself.

I am not stating what is not already obvious here. I am only saying that It is necessary to eliminate from the pool of potential investees, those projects that are discreetly confined toward particular business models.

Once you have weeded out these lazy models, one must ask the real question,” why do I think this investee would be given to change and venturing into new fields.” If he acts for the right reasons, and not because he is shifty or uncomfortable with seeing through what he stared, then we are more likely be looking at a good investment.

But, first we must avoid investments confined in their models, and then we must ask why those that are not confined are not confined. The former question promotes profit—the latter question promotes safety. Purpose, Vision and Trust are the essential ingredients.

Posted by Bill Churchill