|

| From Upside/downside graphs |

|

| From Upside/downside graphs |

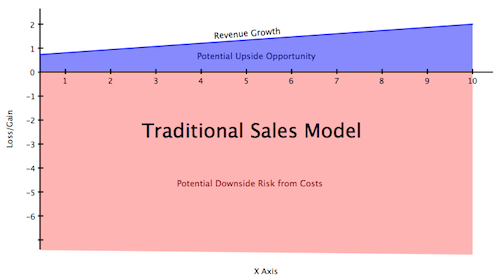

Over the years, Reid Hoffman and I have talked a lot about venture investing and the things that make people successful in startups. Reid likes to doodle a little graph on paper napkins about downside vs. upside focus and I thought I'd expand that a bit and share.

Normal sales oriented companies and organizations have sales that grows month on month if the organization is doing well. While there is a tremendous amount of energy spent on increasing sales, typically sales are capped by some reasonable growth rate over time.

On the other hand, the downside of a company is nearly unlimited. Projects can cost nearly an infinite amount of money if mismanaged and there are a myriad of risks that can cost an operating company tons of money.

The larger and more established the company, the more the organization, as a whole seems to be focused on mitigating risk and minimizing costs as a way to increase earnings and protect itself.

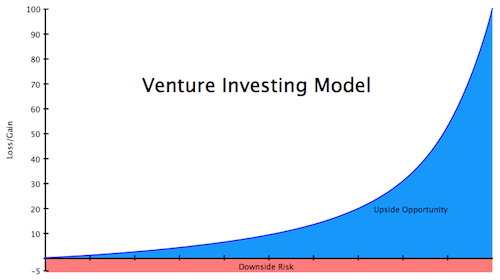

Venture investing, on the other hand, is typically a fund or an individual with relatively limited downside. The most that you're going to lose is the money you've invested and your time.

The upside in venture investing, however, is hugely leveraged. If you're in a good deal, you can make hundreds and thousands times your money with very little incremental cost. The key is to make sure you're in the right deals and that those companies that will potentially knock the ball out of the park get all of the help and support that they need to maximize their chance of success.

In fact, most successful investors spend the majority of their time working on their successful portfolio companies and very little time on the companies that are doing poorly.

In many cases, the companies that are doing poorly need the most help and the intuition is to focus on protecting our investments. Many investors spend all of their time helping their poorly performing companies.

I think that the training from traditional businesses causes people to focus on minimizing the downside instead of single-mindedly focusing on the upside. However, in a venture investment, the MOST you will lose is the money you have invested. Getting 1 million of the 5 million that you invested back from a liquidation is not nearly as important as making sure you're in the next big hit and that the investments that have potential achieve their potential and find their acquirers and partners.

This also influences the way people negotiate contracts. A few percentage points or deal points here and there can damage, slow down or destroy relationships and businesses. Trying to get every last percentage point out of a transaction with a startup is fighting over something that's worth zero if the company isn't successful. It's much more likely to increase your chance of making money if you're helpful and supportive than if you've pushed the entrepreneur against the wall and taken every last percentage point out of the deal that you can from them.

It's stupid to be a sucker and it's not prudent to be sloppy, but squeezing entrepreneurs unnecessarily for that extra nickel isn't worth it when the probability of upside is what you're trying to increase and having more rights in a failure is really not going to make you rich.

I think that all good investors understand this focus on upside vs. downside and I struggle with partners, co-investors and entrepreneurs who seem to live in a downside minimization model. Downside minimization may save you money here and there, but over the long run, will never really provide the kind of returns that an upside oriented model will.